Achieving real and sustainable competitive advantage requires a clear understanding of what “competitiveness” means and how to analyze it effectively. Such clarity is the key to creating economic environments that boost innovation, efficiency and prosperity.

Competitivenss is determined by the productivity with which a location uses its human, capital, and natural endowments to create value.

Productivity ultimately depends on improving the microeconomic capability of the economy.

It is not what a location competes in that determines its prosperity, but how productively it competes.

Every business operates within a playing field—the environment where it is born and where it learns to compete. The diamond is a model for identifying multiple dimensions of microeconomic competitiveness in nations, states, or other locations, and understanding how they interact.

By identifying and improving elements in the diamond that are barriers to productivity, locations can improve competitiveness.

Businesses create jobs and wealth, not governments.

Many things matter for competitiveness. Successful economic development is a process of successive upgrading, in which the business environment improves to enable increasingly sophisticated ways of competing. This environment is embodied in four broad areas as captured in the diamond model.

Conditions of production factors such as specialized labor, natural resources, and infrastructure that influence a firm's competitive advantage.

The strategies, organizational structures, and the intensity of local rivalry between firms — factors that push companies to improve and innovate.

Presence of supplier industries and related sectors that are internationally competitive; strong clusters support faster diffusion of innovation.

The nature and size of domestic demand for the industry's products and services; how sophisticated or demanding customers are drives innovation and quality.

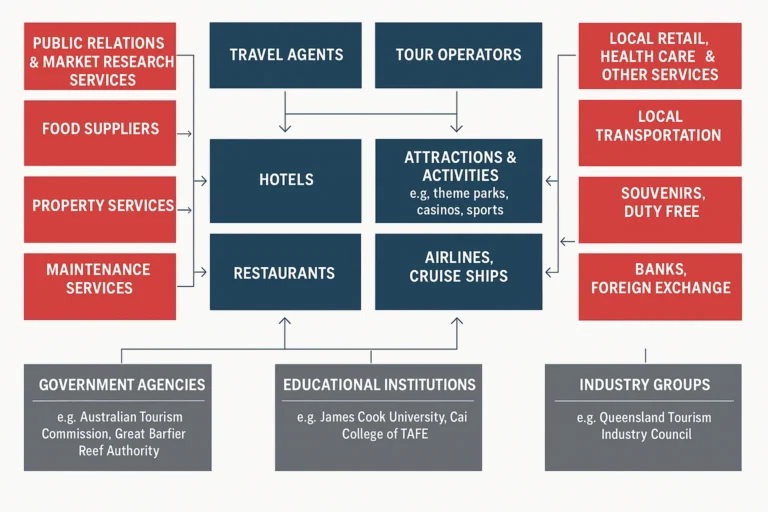

Today’s economic map of the world is characterized by “clusters.” A cluster is a geographic concentration of related companies, organizations, and institutions in a particular field that can be present in a region, state, or nation. Clusters arise because they raise a company’s productivity, which is influenced by local assets and the presence of like firms, institutions, and infrastructure that surround it.

Tourism Cluster in Cairns, Australia

In Cairn, this cluster (a group of interrelated businesses and institutions) was built around the Great Barrier Reef. Other examples of clusters include the Italian Footwear and Fashion Cluster, the California Wine Cluster, and the Silicon Valley Technology Cluster.

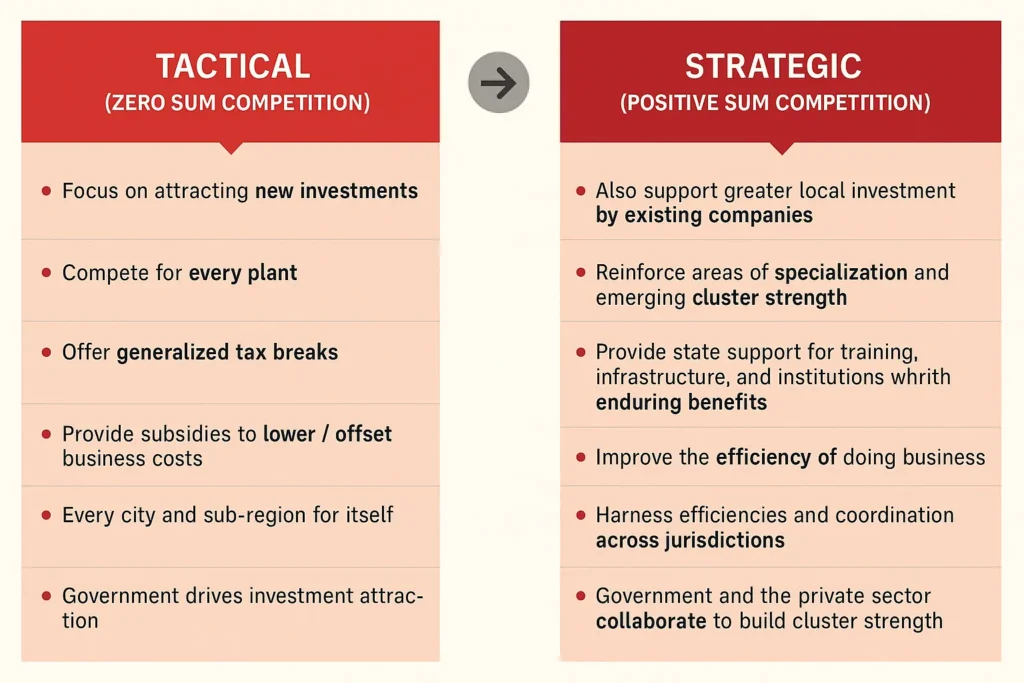

Nations, regions, states, and cities all require clear economic strategies that engage all stakeholders, boost innovation and ultimately improve productivity. A collaborative strategy—which is especially critical in times of austerity or economic distress—requires setting priorities and moving beyond long lists of discrete recommendations.

The value proposition defines the distinctive competitive position of the area given its assets, location and potential strengths.

Capitalism is suffering from a crisis of trust. Today’s businesses take the blame for many of society’s economic, social and environmental woes, despite the launch of countless corporate social responsibility initiatives in recent decades. Now more than ever—in the midst of a global economic crisis that has strained the capacity of governments and NGOs to address complex societal challenges—it is time to restore public trust through a redefined vision of capitalism with the full potential to meet social needs.

The next transformation of business thinking lies in the principle of shared value: creating economic value in a way that also creates value for society by addressing its needs and challenges.

What is shared value? Corporate policies and practices that enhance the competitive advantage and profitability of the company while simultaneously advancing social and economic conditions in the communities in which it sells and operates. Shared value is not corporate social responsibility, philanthropy, or even sustainability, but a new way to achieve economic success.

Evolving Approaches

Companies can create economic value by creating societal value. There are three distinct ways to do this: by reconceiving products and markets, redefining productivity in the value chain, and improving the local and regional business environment. Each of these is part of the virtuous circle of shared value. Improving value in one area gives rise to opportunities in the others.

All strategy is based on understanding competition. Michael Porter’s frameworks help explain how organizations can achieve superior performance in the face of competition. Strategy defines the company’s distinctive approach to competing and the competitive advantages on which it will be based. A good competitive strategy is one that creates unique value for a particular set of customers.

Strategy is the creation of a unique and valuable position, involving a different set of activities.

Strategy involves creating “fit” among a company’s activities.

Competing to be the Best vs. Competing to be Unique

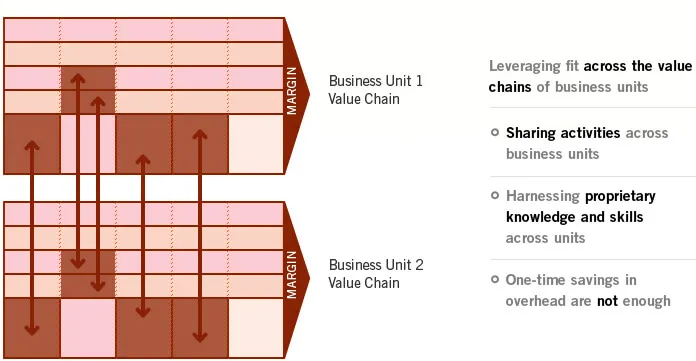

Big companies aren’t necessarily more successful than small ones. Growing, acquiring, diversifying—none of these actions guarantees superior economic performance. Companies compete at the level of individual businesses, where strategic positioning within an industry creates value for customers. Successful strategy at the corporate level must produce a clear and significant benefit to the competitive advantage of business units.

In diversified companies, corporate leaders can enhance competitive advantage by capturing synergies and harnessing fit across the value chains of business units within the corporate portfolio.

In Cairn, this cluster (a group of interrelated businesses and institutions) was built around the Great Barrier Reef. Other examples of clusters include the Italian Footwear and Fashion Cluster, the California Wine Cluster, and the Silicon Valley Technology Cluster.

Developed by Michael Porter and used throughout the world for nearly 30 years, the value chain is a powerful tool for disaggregating a company into its strategically relevant activities in order to focus on the sources of competitive advantage, that is, the specific activities that result in higher prices or lower costs.

A company’s value chain is typically part of a larger value system that includes companies either upstream (suppliers) or downstream (distribution channels), or both. This perspective about how value is created forces managers to consider and see each activity not just as a cost, but as a step that has to add some increment of value to the finished product or service.